Before I ever experienced financial independence, I made a decision that most people around me would not have chosen.

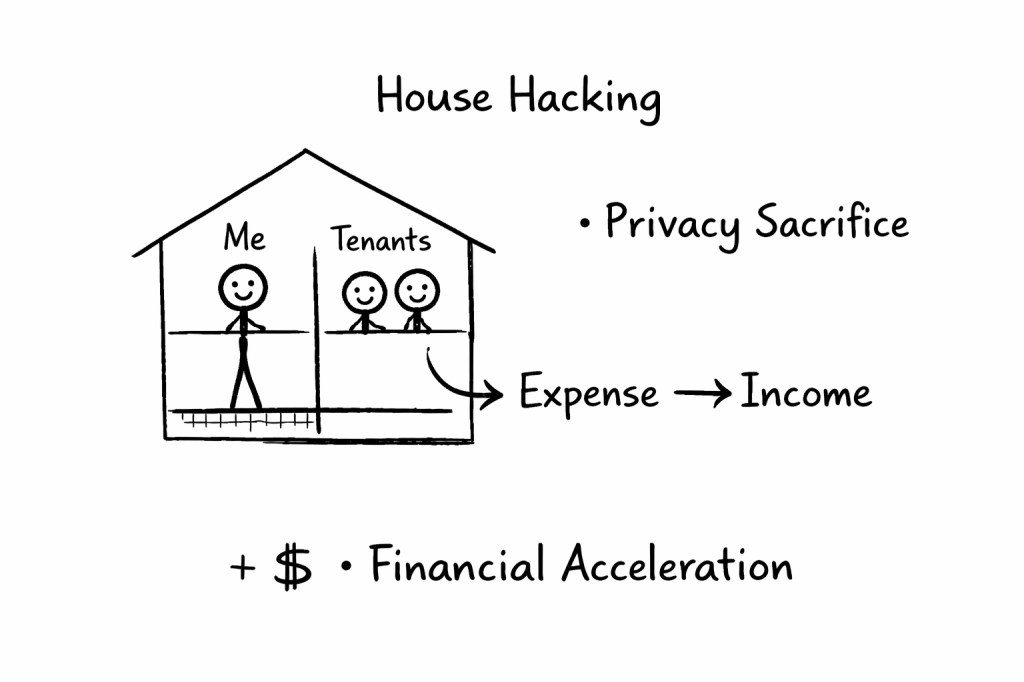

I lived with my tenants.

Not metaphorically.

Literally.

My wife and I shared a house with the people who were paying rent.

That decision accelerated everything financially.

But it also demanded something from me that money books rarely talk about:

Privacy.

Why I Did It

After writing down my financial statement and setting clear targets, one thing became obvious.

Housing was my largest expense.

If I could turn that expense into income, the numbers would move much faster.

So I bought a property and structured it in a way that allowed us to live in part of it while renting out the other parts.

This is often called “house hacking.”

For me, it wasn’t a clever strategy.

It was a math decision.

The Rule Behind It

The rule was simple:

If I can reduce my largest expense while building an asset at the same time, I do it.

Living with tenants dramatically reduced our living costs.

In some months, it almost eliminated them.

That changed the trajectory of our financial statement immediately.

What It Cost Me

Privacy.

You cannot fully relax when you share walls with people who are also your tenants.

There is responsibility.

There is awareness.

There are maintenance issues.

There are personalities.

And there is the constant need to think not just like a resident, but like an owner.

That shift changes you.

You stop thinking only about comfort.

You start thinking about sustainability.

What It Taught Me

House hacking forced me to become:

- A better communicator.

- A clearer negotiator.

- A more patient problem solver.

- More structured with contracts and expectations.

Unexpected problems happened.

Water leaks.

Repairs.

Tenant concerns.

There were no ready-made solutions.

Every issue required calm thinking.

And because I lived there, I couldn’t emotionally detach from it.

That was uncomfortable.

But it built competence.

The Long-Term Shift

Even now, I no longer live in the same property as my tenants.

But managing property remotely comes with a different kind of responsibility.

I must think like an employer.

I hire contractors.

I communicate clearly.

I solve problems without being physically present.

House hacking was not just a financial strategy.

It was leadership training.

What This Did For My Financial Path

Reducing my largest expense allowed me to:

- Increase savings.

- Increase investments.

- Accelerate asset accumulation.

- Build financial stability faster than income increases alone would have allowed.

It was not glamorous.

It required sacrifice.

But it moved the numbers.

And the numbers do not lie.

Would I Recommend It?

Only if you understand the tradeoff.

You gain financial acceleration.

You lose some comfort.

If privacy is non-negotiable for you, this path may not be worth it.

But if your priority is financial momentum, it is one of the strongest levers available.

If you want to experiment with this idea, start by asking:

What is your largest recurring expense?

And is there a way to convert part of it into income?

You don’t need a perfect plan.

You need to see the lever.

If this resonates with you but you’d rather not comment publicly, feel free to reach out through my contact page. I read every message personally.

Leave a comment