For many years, I spent first and saved later.

In my twenties and early thirties, money flowed in and flowed out just as easily. I didn’t feel irresponsible. I simply didn’t think long term.

Then one day in my mid-thirties, I looked at my numbers and realized something uncomfortable.

If I lost my job, I wouldn’t last a month.

I had little to show financially for years of working.

That realization brought worry and stress. But looking back, it was also one of the best wake-up calls of my life.

In my previous post, I explained my financial backbone: the personal financial statement. But clarity alone is not enough.

You need structure that runs even when motivation disappears.

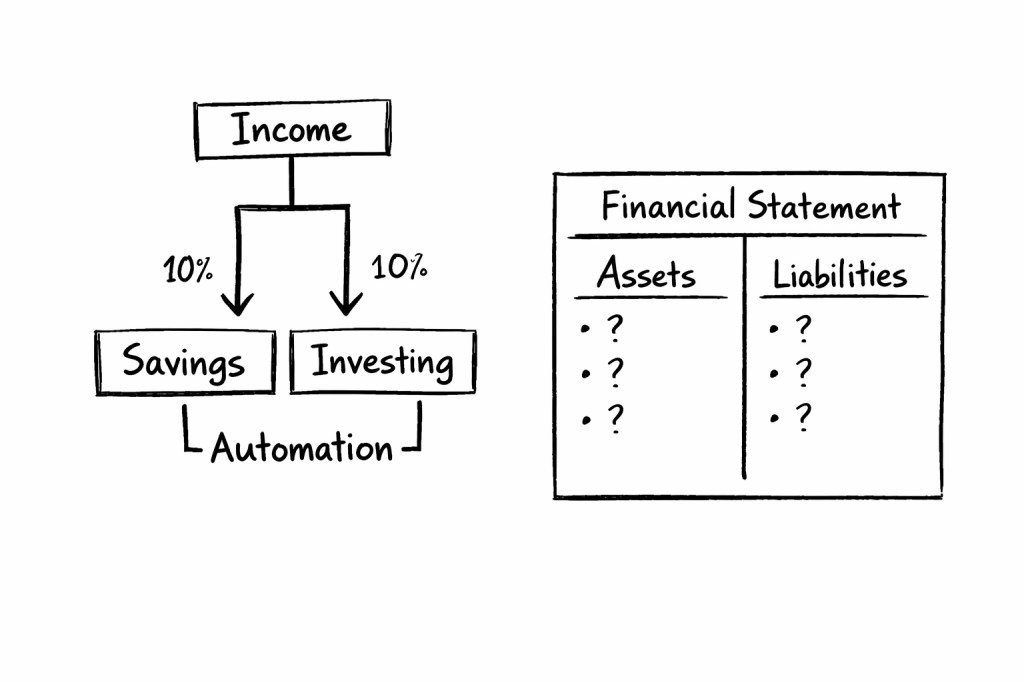

The Rule I Installed

After writing down my financial statement, I created a simple rule:

On every payday:

- 10% goes to savings.

- 10% goes to investments.

No discussion. No negotiation. No “this month is special.”

It wasn’t exciting. It was automatic.

And that was the point.

Why Automation Matters

Saving manually requires discipline every month.

Automation removes that friction.

The moment income arrived, allocation happened.

I didn’t need to decide. I just needed to maintain.

That reduced stress almost immediately.

Because progress stopped depending on my mood.

The Platform and The Action

I did basic research online, watched financial content, and opened an investment account. For me, it was DeGiro.

Opening the account took less than 30 minutes.

I started investing in dividend stocks because I wanted income-producing assets, not just price appreciation.

Was I an expert? No.

I started simple.

Google Finance.

Dividend.com.

Basic research.

Buy and hold.

That’s it.

Nothing sophisticated.

What I Learned About Risk

Investing is risky. I lost money along the way.

But something important happened:

The more I invested consistently, the clearer I became about my own risk tolerance.

I learned:

- How I react to volatility.

- How I respond to loss.

- How patient I really am.

That self-knowledge is more valuable than any stock tip.

Saving Is Not Enough

At first, I believed saving alone would protect me.

Saving is essential for a buffer.

But saving alone does not outpace inflation.

Investing is not a replacement for saving. It is an addition.

One builds stability.

The other builds growth.

Both together build resilience.

Where The Compounding Became Visible

The real shift happened when dividends started accumulating.

Instead of spending them, I reinvested them.

More assets.

More dividends.

More assets again.

That cycle is slow at first.

Then it becomes noticeable.

And over time, it becomes structural.

Not magic.

Just repetition.

What This System Did For Me

It replaced financial anxiety with measurable progress.

It created consistency without constant effort.

It forced me to think long term.

And most importantly:

It allowed me to build financial security while still living my life.

If you want to experiment with this, start simple.

Choose a percentage that feels sustainable.

Automate it.

Let it run.

You don’t need perfect knowledge to begin.

You need a rule.

And then you need to follow it.

If this resonates with you but you’d rather not comment publicly, feel free to reach out through my contact page. I read every message personally.

Leave a comment